Auto Loans Calculator

June 14, 2024

June 14, 2024

April 5, 2024

How can you get closer to achieving your financial goals? Depending on your income, assets, investments, and personal knowledge of finance, you may feel you can do a great job managing your money on your own. But according to a recent report from Boston research firm Cerulli Associates, the number of Americans willing to pay for financial advice has increased from 38 percent in 2009 to 63 percent in 2022. Why are more clients seeking help, how can a financial advisor make a difference, and is the advice worth the cost? Let’s explore answers to these questions.

There are many reasons why you might need a financial advisor:

Complex investment options. As the financial landscape changes, there are many more choices to make regarding investments, along with new regulations that may be difficult to navigate without professional guidance.

Aging baby boomers. A large percentage of the population is nearing retirement and seeking help to figure out how to maximize their savings to live comfortably after ending their careers. Longer life expectancies have also made retirement planning and guidance more important across age groups.

Economic factors. In times of market volatility, financial guidance becomes especially important. Inflation was a big concern for many people in 2022. Financial advisors can help answer questions like “will rising inflation affect my goal of retiring in the next 10 years, or do I need to adjust my portfolio to better keep up?”

The Benefits

There are many ways a financial advisor can offer value and assistance you may not be able to achieve on your own.

Saving time, reducing stress, and avoiding mistakes. Sure, you can do all the research, but having professional advice you trust and a knowledgeable person to ask when you’re unsure takes much less time and reduces the anxiety of trying to get it right on your own. In addition, working with an advisor can help you avoid making critical financial mistakes (e.g., taking on an inappropriate level of risk within your portfolio for your investment goal), which can be costly and detrimental to your financial plans.

Professional advice. Even if you devote time to doing your own financial research, an advisor likely has a more comprehensive financial education and more investing experience than you have. The experience an advisor brings can inform your strategies and get you closer to achieving your financial goals.

Staying on track. Regular check-ins with your advisor can help keep you on course toward your financial goals, keep track of your progress, and adjust your saving and investing strategies when necessary.

Comprehensive planning. Although you may have the resources to study new investment options or specific savings tools such as IRAs or 529 plans, it would be time-consuming to master the wide-ranging planning strategy that a financial advisor could help you create. In addition to asset accumulation, an advisor can provide insight into budgeting, saving, retirement planning, estate planning, tax planning, debt management, risk management, and business planning.

Possible access to connections. Advisors may collaborate with a network of attorneys, CPAs, insurance agents, and other professionals who can work together to help you achieve your goals.

How to Evaluate and Choose an Advisor

The best way to begin your search for a financial advisor is to ask family and friends for recommendations. If someone you know and trust vouches for the advisor, of course, there’s a better chance of finding a good match versus choosing one at random. So, what should you look for when choosing an advisor to help guide your financial decision-making?

Firm affiliation, experience, and certification. Just as you would evaluate the résumé of a potential hire, you should evaluate the education and background of a potential financial advisor. If your advisor has designations, research them and find out what the requirements were for obtaining them. Some designation requirements are more rigorous than others. You may want to look for continuing education, any examination requirements and adherence to a code of ethics.

Fee structure. Some financial professionals collect commissions based on the investments they pick or the products they sell you. Others charge a flat fee or a percentage fee based on assets under management regardless of their recommendations or your investments. Be sure to ask about your financial advisor’s fee structure and how they get paid.

Trust and personal attention. Your advisor should give you as much information as you need to make the best financial decisions for you and your family. So, it’s important to feel your advisor is listening to you, considering your circumstances and needs, and making recommendations you trust.

The Value

Whether working with a financial advisor is worth the cost depends on several factors. You may consider whether the potential investment growth you expect will be more than the advisor fee, but that’s not the only consideration. As the saying goes, time is money. So, the time you may save if you don’t have to educate yourself about various aspects of financial planning and investing should also factor into the benefit. You can also consider the benefits of working with a financial planning professional over time for things such as retirement planning, saving for education, and tax planning. Finally, the sense of financial security a trusted advisor can provide is priceless to some.

If you, a friend, or family member is considering working with a financial advisor, we’d love to hear from you. As always, we aim to provide support and help you reach your financial goals.

© 2024 Commonwealth Financial Network®

Want to pay less taxes? If given a way to legally reduce tax liability, most Americans would welcome that opportunity with open arms. But methods for doing so aren’t always obvious—and may be tricky in certain circumstances. Two such situations include working in the gig economy and navigating required minimum distributions (RMDs) from retirement accounts. Let’s explore strategic tax planning options for both cases.

Tax Planning for Gig Workers

The gig economy refers to the rise in freelance work through apps such as Uber, TaskRabbit, DoorDash, and Etsy. As a gig worker, you have the flexibility to work on your own time and be your own boss, but you’re responsible for managing your income, expenses, and tax obligations. This could prove difficult and time-consuming, especially if you aren’t well-versed in tax law. There are ways, however, for freelancers to reduce their tax burden and comply with IRS rules and regulations.

Using RMDs for Tax Planning in Retirement

As baby boomers retire and life expectancy increases, tax planning for retirement is becoming increasingly important for American workers. One way to maximize tax savings in retirement is through RMDs. You’re required to take RMDs from certain retirement accounts the year you turn 73. Withdrawing them, however, could result in a large tax bill because these are considered taxable income. Here’s how to cut down on what you’ll owe.

Reducing your tax bill sounds great, but it requires careful planning and understanding of tax laws. Whether you’re a gig worker hoping to take advantage of deductions, a retiree trying to use RMDs to your advantage, or you’re looking at another possible way to legally reduce what you owe the IRS, please reach out to us. We’d love to help with your strategic tax planning. As always, we aim to help you make the most informed decision to optimize your financial well-being.

This material has been provided for general informational purposes only and does not constitute tax, legal, or investment advice. Although we go to great lengths to make sure our information is accurate and useful, we recommend you consult a qualified professional regarding your situation. Commonwealth Financial Network does not provide tax or legal advice.

© 2024 Commonwealth Financial Network®

An increasing number of women are becoming primary breadwinners in their households, so one might assume women are also taking on most of the financial decisions. On the contrary, most women in heterosexual relationships who are earning more of the household income aren’t making the major money-related decisions for the family1. So, why doesn’t earning power naturally lead to financial decision-making power?

While these reasons might all play into women’s lack of involvement in family finances, it’s critical for women to be in the know about where their money is going. Why? Women are often paid less than their male counterparts, which makes it more challenging for them to save for the future and achieve financial stability. Women are also more likely to take career breaks or work part-time to care for children or elderly parents, which comes with its own financial responsibilities. This can result in lower income and less retirement savings. Finally, women tend to outlive men, which means they need to save more for retirement and plan for a longer lifespan. For all these reasons, female breadwinners should budget strategically, prioritize their retirement planning, and plan for unexpected expenses and emergencies, such as medical bills or home repairs. To manage your finances more effectively and help you achieve your long-term goals, follow these tips for female breadwinners.

Tips to Take Charge

Communicate openly. Establishing open communication with your partner about financial goals, responsibilities, and expectations is key. This might also include redistributing household responsibilities—either to your partner or to an outside person or service—to allow more time for you to help manage your family’s money. Consider planning a date night to discuss your finances to help diminish any relationship tension around the subject.

Compile important information. As part of your communication with your partner about finances, it will be helpful to gather all your account numbers, names of financial institutions, location of assets, passwords, and important contacts such as attorneys and CPAs in one place. You should have hard and digital copies, and your trusted family members should know where they’re located. In the event one of you passes unexpectedly, having this will make a difficult situation slightly less complicated to navigate. Ask your financial advisor if they have a template for this type of document that requires you to just fill in the blanks.

Create a budget. This will help you track your income and expenses, identify areas where you can cut back, and plan for the future. Start by listing all your monthly income and expenses, including bills, groceries, and other necessities. Having a clear sense of where your money is going will help you identify areas for improvement and is the first step toward becoming more involved in managing your family’s finances.

Save for retirement. Women need to save a larger percentage of their income for retirement than men just to end up at the same level of wealth. This is because women often take time out of the workforce, make less money than men, and live longer on average. So, retirement planning is crucial, especially if you’re the primary breadwinner. Make sure you’re contributing enough to your retirement accounts, such as 401(k)s or IRAs, and consider working with a financial advisor to determine the best investments for your goals.

Start an emergency fund. There’s always a chance you may face unexpected expenses, such as medical bills or home repairs. Having a financial safety net can alleviate stress, avoid a financial challenge, and provide a sense of security.

Purchase insurance. Ensure that you and your family have adequate coverage, including health, life, and disability insurance. These protect against unexpected events that could jeopardize your family’s financial stability.

Get your estate documents in order. In addition to a fund for emergencies and setting up insurance coverage, you’ll want to plan for your family’s future in case something happens to you. It’s advisable to consult with a qualified attorney about your specific situation and unique goals. Core estate planning documents generally include:

You’ll also want to update your beneficiary designations. Outdated beneficiary designations can derail an estate plan. Review your designations periodically to ensure that the correct people are named and are still appropriate.

Learn about personal finance. If you feel a lack of confidence in making financial decisions, attend workshops, read books, or consult with financial advisors to enhance your understanding of investments, retirement planning, and other financial instruments. Better understanding will lead to a greater sense of comfort in managing your money.

Consult a financial advisor. A professional can help you in various ways, such as informing you about tax breaks or credits you might not have known about, choosing investments based on your risk comfort level, and setting up the most beneficial retirement plan for your needs.

As more women take on the role of breadwinners in their families, they face unique financial challenges. With careful planning and management and communication with your partner, you can achieve financial stability and help ensure a secure future for yourself and your loved ones.

This material has been provided for general informational purposes only and does not constitute tax, legal, or investment advice. Although we go to great lengths to make sure our information is accurate and useful, we recommend you consult a qualified professional regarding your situation. Commonwealth Financial Network does not provide tax or legal advice.

© 2024 Commonwealth Financial Network®

The “great wealth transfer” is set to take place over the next two decades, when baby boomers (the wealthiest generation in American history) will pass $30 trillion down to younger generations. One common asset many aging parents will look to transfer or sell is their home, especially if they feel compelled to downsize or need to move due to declining health. If you’re planning to purchase, transfer, or inherit your parent’s home, there are many factors to consider. Here are eight things to think about to make the process smoother and less taxing—both emotionally and financially.

Personal Considerations

Regardless of how many years your parents have spent in their current home, it’s made up of so much more than floors, walls, and windows. Any family home comes filled with memories and emotional attachments, so your first consideration should be your parent’s wishes and feelings about passing down their property. Communicating openly about their preferences and needs will help them feel supported in their decision, set the stage for a smoother transition, and help align your family members’ expectations.

If there are other siblings or heirs involved, it’s helpful to address their concerns and interests, too. Open communication, transparency, and potentially seeking the assistance of a mediator can help alleviate any conflicts or resolve differing opinions about the future of your family’s home.

Although sentimental value is a strong reason for many to want to buy or transfer a parent’s home, it’s crucial to consider the long-term implications. First, do your parents have funds to pay for their care needs, especially if they will be moving to a nursing home or assisted living facility? Do they have enough income for rent if they’re downsizing? Also, do you have the funds to maintain the home? If it’s a multifamily home or has rental units, are you prepared to be a landlord? Consider future scenarios before you finalize the decision. You may want to consult a financial advisor for guidance.

Financial Considerations

One of the biggest concerns when transferring or purchasing a home is the potential tax liability. Depending on the value of the property and the circumstances of the transfer, there may be gift tax, estate tax, or capital gains tax implications to consider. It’s important to consult with a tax professional to understand the specific tax implications of any transaction, explore strategies for minimizing tax liabilities, and ensure compliance with current tax laws.

Transferring or selling a home can also affect eligibility for certain government benefits, like VA pensions or Medicaid. This is because these programs have strict asset and income limits, and transferring or selling a home can affect those limits and, therefore, impact qualification for those benefits. Consult with an attorney or financial advisor who specializes in elder law to understand the potential impact and explore options for protecting these benefits.

Probate is the legal process of distributing a person’s assets after they pass away, and it can be time-consuming and expensive. One option for avoiding probate is transferring the home into a living trust. This way, you can ensure a smoother, simpler transfer of ownership after your parents pass on, minimizing the burden on their heirs. There are several types of trusts, each with its benefits and drawbacks. It’s important to consult with an estate planning attorney to determine which type of trust is best for your specific situation.

In addition to the tax considerations, it’s important to budget for mortgage rates, closing costs, transfer fees, appraisal fees, and the expense of ongoing maintenance.

Many families are afraid they need to sell their parent’s home to cover the costs of long-term care, but this may not be true. There are alternatives to selling, such as accessing home equity through a reverse mortgage or purchasing insurance for long-term care expenses. Careful financial planning, possibly with a professional, can help preserve the family home while addressing the financial demands of care.

Transferring or purchasing your aging parent’s home can be a complex process, with many legal and financial considerations to keep in mind. By working with qualified professionals, such as attorneys, financial advisors, and tax professionals, you can ensure that the process is done correctly and in the best interests of all parties involved.

© 2024 Commonwealth Financial Network®

Market Update—Quarter Ending March 31, 2024

Posted April 4, 2024

Strong Start to the Year for Stocks

It was a positive March for stocks, capping off a strong quarter to start the year. The S&P 500 gained 3.22 percent in March and an impressive 10.56 percent in the first quarter. The Dow Jones Industrial Average was up 2.21 percent during the month and 6.14 percent for the quarter. The Nasdaq Composite lagged its peers during the month but still had a strong start to the year, with a 1.85 percent gain in March and a 9.31 percent rise for the quarter. Improving fundamentals and a healthy economic backdrop helped drive the gains in the first quarter.

Per Bloomberg Intelligence, as of March 29 with all companies having reported earnings, the average earnings growth rate for the S&P 500 in the fourth quarter was 8.3 percent. This is notably higher than analyst estimates at the start of earning’s season for a more modest 1.2 percent increase. The better-than-expected earnings growth was widespread with 10 of the 11 sectors coming in above analyst estimates. Over the long run fundamentals drive market performance, so the impressive earnings growth was a good sign for investors.

Technical factors were also supportive during the month and quarter. All three major U.S. indices spent the entire quarter above their respective 200-day moving average. The 200-day moving average is a widely monitored technical indicator as sustained breaks above or below this level can signal shifting investor sentiment for an index. The continued technical support throughout the quarter was another welcome development for investors at the start of the year.

Results were similar, albeit a bit more muted, for international equities. The MSCI EAFE Index gained 3.29 percent in March and 5.78 percent for the quarter. The MSCI Emerging Markets Index rose 2.52 percent in March, but weakness to start the year held back quarterly results for emerging markets as the index only gained 2.44 percent for the quarter. Technical results were mixed for international stocks, as the MSCI EAFE Index spent the entire quarter above its 200-day moving average, while the MSCI Emerging Markets Index briefly fell below trend at the end of January before rebounding above its trendline for the rest of the quarter.

Mixed Quarter for Bonds

While equities had a largely positive start to the year, results were more mixed for fixed-income investors. Rising interest rates throughout the quarter weighed on bond prices, leading to a choppy ride for fixed-income markets. The 10-year U.S. Treasury Yield rose from 3.95 percent at the start of the year to 4.20 percent at the end of the quarter. The Bloomberg U.S. Aggregate Bond Index managed to notch a solid 0.92 percent gain in March, but the index was still down 0.78 percent for the quarter.

High-yield fixed income, which is typically less sensitive to changing interest rates, held up better during the month and quarter. The Bloomberg U.S. Corporate High Yield Index gained 1.18 percent in March and 1.47 percent for the quarter. High-yield credit spreads started the year at 3.54 percent and ended March at 3.12 percent. Falling credit spreads are a sign that investors became more willing to invest in the relatively riskier portions of the fixed income market during the quarter.

Healthy Economic Growth

The economic updates released throughout the quarter showed signs of healthy economic growth to start the year. Hiring accelerated at the end of 2023 and the momentum has carried into 2024, as more than 500,000 jobs were added between January and February. This strong job growth helped support continued personal income and spending growth, with personal spending rising in February at the fastest monthly pace in over a year.

Business spending also rebounded in February, following a Boeing-related slowdown in aircraft orders in January. Core durable goods orders, which strip out the impact of volatile transportation orders, also rebounded well in February after falling in January. This improvement was driven in part by improving manufacturer confidence and supportive service sector confidence to start the year. The improvement in manufacturer confidence was especially encouraging as the ISM Manufacturing Index rose into expansionary territory for the first time since 2022, in March.

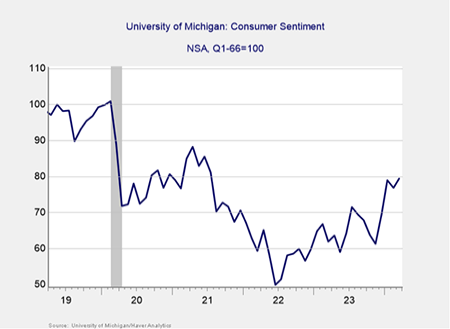

We also saw improving consumer sentiment during the quarter, which is a good sign for future consumer spending growth. As you can see in Figure 1 below, the University of Michigan Consumer Sentiment Index ended March at its highest level in over two years. Improved consumer views on current economic conditions as well as future expectations helped power the improvement in sentiment that we saw throughout the quarter.

The Takeaway

Inflation and the Federal Reserve

While the strong economic growth to start the year was largely welcome for investors and economists, one downside of the better-than-expected growth was that it helped keep inflation stubbornly high during the quarter. We ended February with both headline and core inflation still well above the Fed’s 2 percent target. Additionally, it appears the progress we saw in late 2022 and throughout much of 2023 in getting inflation down has started to slow, with headline and core inflation only seeing modest improvements in the first quarter.

Given the still high levels of inflation, the Fed left rates unchanged at both their January and March meetings. Fed chair Jerome Powell reiterated the Central Bank’s commitment to getting inflation back down to 2 percent at the Fed’s March meeting and markets have adjusted their expectations for the Fed throughout the start of the year.

We entered the year with futures market pricing in roughly six interest rate cuts throughout the course of 2024, with markets calling for the first rate cut in March. Since then, we’ve seen job growth remain resilient while inflation has remained high, causing markets to pare back their expectations to be more in line with the three rate cuts the Fed expects by the end of the year. While these repriced expectations weighed on bonds to start the year, they should help keep volatility in check going forward provided we don’t see a further rise in inflation.

The Takeaway

Market Risks Worth Monitoring

While a healthy economic backdrop and improving fundamentals helped propel markets to new highs in the first quarter, real risks remain for investors. The ongoing conflicts in Ukraine and the Middle East are one such risk. While the direct market impact from these clashes has remained muted, they have the potential to snarl already tangled global supply chains and drive further inflationary pressure, especially if hostilities escalate in these volatile regions.

Domestically the largest market risk is a potential reacceleration in inflation. While investors and markets have done well to lower their expectations for rate cuts this year, a sustained uptick in inflation could cause the Fed to wait until we see further improvement on the inflation front before cutting rates. The upcoming election in November is also a worth watching, as it will likely serve to drive uncertainty later in the year.

Other risks to monitor include a slowdown in China, relatively high valuations for U.S. stocks, and rising investor complacency. As always, the potential for unknown risks to negatively impact markets remains. As we saw last month with the destruction of the Francis Scott Key Bridge in Baltimore, external events can rear up at any time and place, with the potential to drive short-term uncertainty.

The Takeaway

Despite the Risks, Outlook Remains Positive

While it’s important to acknowledge the current market risks, overall we remain in a relatively good situation with a positive outlook for the months ahead.

The economic backdrop remains largely supportive, powered by a resilient job market that in turn helps drive improved consumer and business activity. U.S. companies have shown an impressive ability to grow earnings and analysts expect to see continued earnings growth ahead. Markets have now readjusted their expectations for the Fed throughout the rest of the year, lowering the potential for Fed-driven pullbacks. And finally we’ve seen encouraging signs that the economic and market momentum from the end of 2023 has carried over into 2024.

Ultimately, things are pretty good right now, but that is not always going to be the case. While continued economic growth and market appreciation remain the most likely path forward, we may face short-term setbacks along the way. Given the potential for short-term uncertainty, a well-diversified portfolio that aligns investor goals with timelines remains the best path forward for most, although if concerns remain you should speak to your advisor to discuss your financial plan.

Authored by Brad McMillan, CFA®, managing principal, chief investment officer, and Sam Millette, director, fixed income, at Commonwealth Financial Network®.

* Diversification does not assure a profit or protect against loss in declining markets, and diversification cannot guarantee that any objective or goal will be achieved

Disclosure: This material is intended for informational/educational purposes only and should not be construed as investment advice, a solicitation, or a recommendation to buy or sell any security or investment product. Please contact your financial professional for more information specific to your situation.

Certain sections of this commentary contain forward-looking statements based on our reasonable expectations, estimates, projections, and assumptions. Forward-looking statements are not guarantees of future performance and involve certain risks and uncertainties, which are difficult to predict. Past performance is not indicative of future results. Diversification does not assure a profit or protect against loss in declining markets. All indices are unmanaged and investors cannot invest directly into an index. The Dow Jones Industrial Average is a price-weighted average of 30 actively traded blue-chip stocks. The S&P 500 Index is a broad-based measurement of changes in stock market conditions based on the average performance of 500 widely held common stocks. The Nasdaq Composite Index measures the performance of all issues listed in the Nasdaq Stock Market, except for rights, warrants, units, and convertible debentures. The MSCI EAFE Index is a float-adjusted market capitalization index designed to measure developed market equity performance, excluding the U.S. and Canada. The MSCI Emerging Markets Index is a market capitalization-weighted index composed of companies representative of the market structure of 26 emerging market countries in Europe, Latin America, and the Pacific Basin. It excludes closed markets and those shares in otherwise free markets that are not purchasable by foreigners. The Bloomberg Aggregate Bond Index is an unmanaged market value-weighted index representing securities that are SEC-registered, taxable, and dollar-denominated. It covers the U.S. investment-grade fixed-rate bond market, with index components for a combination of the Bloomberg government and corporate securities, mortgage-backed pass-through securities, and asset-backed securities. The Bloomberg U.S. Corporate High Yield Index covers the USD-denominated, non-investment-grade, fixed-rate, taxable corporate bond market. Securities are classified as high-yield if the middle rating of Moody’s, Fitch, and S&P is Ba1/BB+/BB+ or below.

© 2024 Commonwealth Financial Network

Posted by Jason Edinger on Tuesday, April 2, 2024

Coming off a robust quarter to conclude 2023, US equities rode the momentum to a series of new all-time highs in Q1, delivering the strongest start to a year since 2019. The S&P500 rose by 10.6% on a total return basis and notched twenty-two record highs during the quarter. While the rally was uniform across the board, small-caps lagged large-caps by a wide margin (Russell 2000 +5.2% vs S&P500 +10.6%) as the market digested a less dovish rate cut environment moving forward. Growth outperformed value, and ten of the eleven GICS sectors were positive during the quarter, with real estate the only sector showing red as of March 31st. To put it mildly, the sailing continues to be smooth.

In contrast to last quarter’s rally – which was a result in large part due to the dramatic fall in bond yields – the extension of gains this quarter came despite a more hawkish repricing of future monetary policy. The Federal Open Market Committee held its benchmark rate constant for the fifth consecutive month (5.25-5.5%) as it seeks more economic data to show “greater confidence” that inflation is on the path toward the magical 2% number. As of this writing, the Fed dots show a projected three cuts in 2024, potentially beginning as early as June or July. This is in stark contrast to the approximately seven cuts seen by the market to begin the new year. With gas prices moving steadily higher to $3.53 per gallon on average, March inflation will be a major influence on the Fed’s decision to begin easing policy.

In terms of economic data, we saw Q4 GDP revised up to 3.4% from its initial 2% consensus, based on a strong consumer who just refuses to stop spending. And why would they? The labor market remains incredibly resilient, with 229K jobs created in January and 275K in February. At the same time, inflation as measured by the Fed’s favorite indicator continues to sink, affirming the goldilocks scenario comprised of cooling inflation, decreasing interest rates, and broadly supportive economic conditions. Not too hot, not too cold, but just right.

Equities are not the only asset class tagging all-time highs as we move into April. Both Bitcoin and gold prices touched unfamiliar territory during the quarter, with the latter now costing more than $2,250 per ounce, up nearly 40% from its recent bottom in 2022. Given gold’s status as a safe haven asset that typically rallies during risk-off markets, this recent uptrend is slightly unusual, but the precious metal continues to increase in value as both the US Dollar and interest rates are projected to fall during the back half of this year. The fact that gold easily blasted through the psychologically crucial $2,000 mark – and has not fizzled – shows that prices appear to be consolidating before the next move.

Finally, during the quarter former and current Presidents Trump and Biden secured enough delegates to clinch the nomination for their respective parties in the upcoming election later this year. While the election has heretofore been relegated to the back burner of investor interest, it should become a key component in future quarters as each candidate’s platform is firmed up, defined, and communicated to the public.

Q1 earnings season is rapidly approaching, and market’s current streak of gains will be highly dependent on those results. The ongoing rally is historic by the true definition of the word, as it is only the ninth time since 1940 that consecutive quarters have delivered back-to-back double-digit gains. Historically, this is a bullish signal and, against the goldilocks backdrop described above, the path to higher returns from here seems clear. However, it is likely that the remainder of the year will be increasingly challenging as the election unfolds and inflation levels bob and weave. Discipline and a sound long-term plan remain critical.

As ever, we thank you for your continued trust and support. Happy spring to all.

All indices are unmanaged, and investors cannot actually invest directly into an index. Unlike investments, indices do not incur management fees, charges, or expenses. Past performance does not guarantee future results.

February 13, 2024

Posted by Jason Edinger on Friday, January 5, 2024

In Review:

Following a tumultuous and disappointing 2022, we faced a fork in the road in terms of what would lie ahead in 2023: a recovery and rally to claw back some or all the previous year’s losses or a continuation of the pain and tough times. It was a deciding moment and may we all be thankful for the road not taken. The market GPS guided in the right direction, and 2023 ended up being a surprisingly strong year for both stock and bond markets.

Despite widespread predictions for a follow-through of the 2022 bear market and an all-but-assured recession, equity performance was impressive. The NASDAQ 100 turned in its best year since 1999 (+55%) while the most widely quoted market index, the S&P500, had an admirable +26.3% year. The Dow Jones underperformed slightly, while small caps enjoyed a furious rally over the final nine weeks of 2023 to conclude the year with a +24.3% mark. All told, equity markets finished 2023 on a high note and on the brink of brand-new all-time highs. It was a good year, and we will take it.

While stocks did most of the heavy lifting, bonds also delivered impressive returns throughout the year. Much attention was paid to the benchmark 10-year Treasury yield, which round-tripped the year to end unchanged after falling as low as 3.3% before ripping up to 5%. All told, the total return on the 10-year note was close to 4% and the aggregate bond index delivered 5.65% of total return in 2023. These returns were achieved despite the Federal Reserve raising interest rates four times throughout the year, capping a 2022 campaign which saw a cumulative 5.25% of aggregate rate increases.

The economy proved exceptionally resilient in 2023. A banking crisis in March resulted in the second largest bank failure in US history, with regional banks selling off nearly 30% in just three trading days. Although steadily decreasing, inflation remained high and the Fed seemed intent on hiking the economy into a recession. Nevertheless, a slew of fiscal and liquidity support was introduced to combat the drag from balance sheet unwinding, an inverted yield curve, and inflation. The labor market was robust throughout the year, as the unemployment rate is holding near generational lows as it appears increasingly likely that the Fed will achieve its highly coveted soft landing. From an economic standpoint, 2023 will be remembered for the recession that never materialized.

In Prediction:

Looking forward, the stage appears set for a continuation of the positive trends that played out in 2023. The economy, far from slowing down or contracting as many economists were convinced would happen, remains robust especially in the areas of job growth, consumer spending, and GDP. The so-called Goldilocks economy – not too soft, not too cold – is likely to set in and act as a foundation for full employment, economic stability, and continuously declining inflation. Against this backdrop, the economy can offer just enough support for financial markets to do well, without the threat of overheating and further potential rate hikes.

Inflation and interest rates will remain important going into the new year, but all signs point to a leveling out (finally). We have seen inflation cool steadily over recent months, largely a result of declining prices for food, energy, and commodities. However, services inflation and shelter (e.g., rent and housing costs) remain high and often operate on a lag, which could support price levels into 2024. In this case, it would be unlikely that the Fed would enact four interest rate cuts during the year as the markets currently predict. While one or two cuts may be in the offing, interest rates are likely to remain elevated as the Fed continues to try and pull inflation down to its 2% target rate.

From political and geopolitical standpoints, we are entering an election year which as always will include its share of fireworks and theatrics. But it is unlikely that the runup to the November vote will influence the financial markets to a large degree. Neither party wants a government shutdown, and even some of the most obstructionist politicians have shown signs of bipartisanship in recent months. More important than the election are policy risks, which include the deficit, debt, taxation and government spending. Any unforeseen developments in these key arenas could reset growth and economic expectations for the new year. Similarly, from a geopolitical view, the takeaway is that we need to be aware of the inherent risks (Ukraine war, Israel-Hamas war, China financial crisis), but markets do a very good job of pricing in such risk and can even rise in the face of them.

As we begin anew, we note that the S&P500 closed out 2023 with nine straight weekly gains, the longest streak since 1985. Ironically, 2023 was also the first year since 2012 that the bellwether index did not register a new all-time high during the period. With the Fed hiking cycle likely behind us, the broad indices are within striking distances of all-time highs. Upside momentum has been broadening in recent weeks, with increased participation, which could be yet another good sign for sustained market performance.

Thank you for your confidence and continued support. Happy New Year, and all the best for 2024.

February 5, 2024

Posted by Jason Edinger on Monday, February 5, 2024

After a strong rally to conclude 2023, the new year rang in with a more cautious tone as small caps slid and large caps led. Stocks have now rallied for the third straight month, marking the longest streak since August 2021. Unlike the last two months, which saw positive returns for both stocks and bonds, this January provided performance dispersion across asset classes, as treasuries experienced weakness with interest rate cuts taking center stage. Small caps also struggled, lagging their large cap brethren and losing nearly 4% of value during the month. Still, strength was seen across the broad indices, with the S&P500 notching a gain of 1.7% and large cap growth names gaining 2.5%. Party on, Wayne.

Mega-cap tech names, to include the vaunted “Magnificent 7,” continued to drive positive performance. Microsoft, a card-carrying member of the Mag7, eclipsed the $3T market capitalization level just as the NASDAQ and S&P500 were making new all-time highs[1]. Despite weakness to begin the month, the overall market direction was higher as the soft-landing scenario was supported by stronger than expected GDP and retail sales numbers which show consumers continuing to defy expectations and spend, spend, spend. This backdrop should support ongoing strength for equities as we move into February.

The treasury yield curve steepened during the month, resulting in modest weakness in the fixed income space. The 10Y treasury yield was essentially flat, but 30Y yields rose as high as 4.4% before pulling back slightly. Broadly speaking, treasury yields behaved as expected after the Federal Reserve left rates unchanged at its January meeting. While the central bank left some options open, it threw cold water on the possibility of a March rate cut, expressing caution about such cuts until there’s more confidence that inflation is moving sustainably toward that magic 2% number. As of this writing, the target rate remains in the 5.25-5.5% range and futures markets are pricing in just a 35% of a March cut. Not great odds for treasury bulls.

Meanwhile, in the “real economy,” both hard and soft data continue to come in strong. The preliminary reading of Q423 GDP was 3.3% annualized, reflecting healthy vigor in the overall economy. The GDP number was driven primarily by personal consumption (contributing 1.9%) and government spending (contributing 0.6%). For the full year, GDP grew by 2.5%, well exceeding expectations. At the same time, the labor market added 3.5M jobs for the full year, resulting in a generationally low unemployment rate of 3.7%. Strong to quite strong.

The one outlier in this slew of bullish data was inflation. The year-over-year pace of inflation ramped up again in December but remains solidly in the 3-4% range that we have observed since May of last year. The reluctantly strong shelter index contributed the most to higher prices, even while core CPI (which strips out select items such as food and energy) eased down to a 3.9% annual pace. Subsequent reports reinforced flat core prices.

Lastly, we did see geopolitical risk increase during the month, as attacks against shipping in the Red Sea by the Houthis are having a dramatic impact on logistics. The implications for global trade and supply chains could be devastating, especially for select areas already reeling from several wars and drought conditions in places like the Panama Canal. Oil prices, as we would presume, rose during January to log their first gain in four months. And while geopolitical factors have failed to materially affect the capital markets in recent years, they remain a wildcard and could easily escalate, along with domestic political uncertainty as the US presidential campaign gears up.

All indices are unmanaged, and investors cannot actually invest directly into an index. Unlike investments, indices do not incur management fees, charges, or expenses. Past performance does not guarantee future results.

[1] Microsoft is now bigger than Apple, and Amazon is now bigger than Google